ETFs Under The Microscope: $RACK

A look at what VanEck's new data center supply chain ETF actually owns, how it's structured, and what the holdings disclosure says about where the bets really are.

VanEck launched the Data Center Supply Chain ETF ticker RACK 0.00%↑ on June 1, 2026. The pitch is straightforward: own the companies building the physical infrastructure for AI, the ones the hyperscalers are buying from. Three weeks in, the fund holds 51 stocks across six categories, with about $26 million in assets (roughly 4x the initial seed capital).

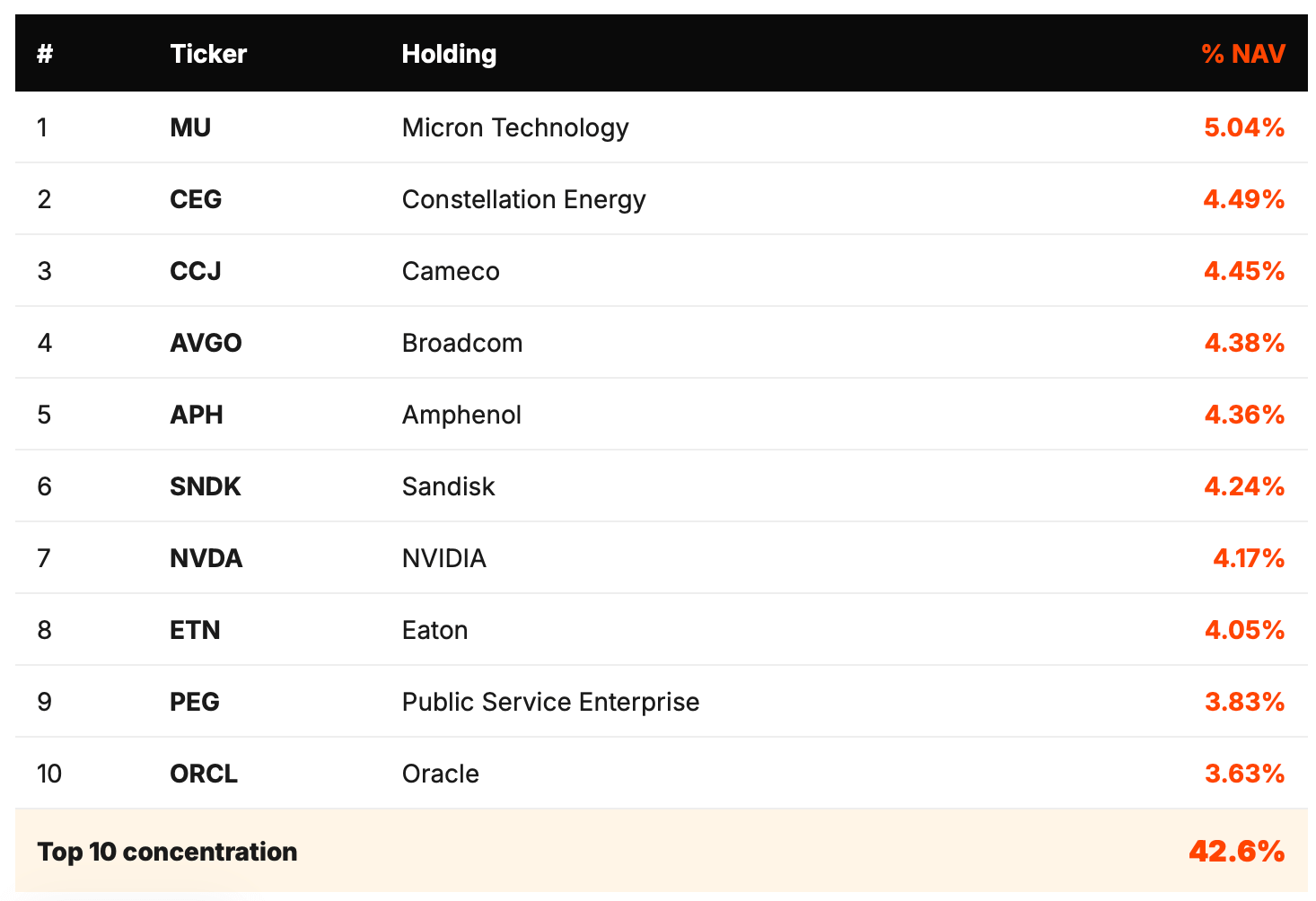

The top five positions tell you where the actual bets are:

Micron Technology (5.04%)

Constellation Energy (4.49%)

Cameco (4.45%)

Broadcom (4.38%)

Amphenol (4.36%).

Memory chips, nuclear power, and grid infrastructure are doing more work in this portfolio than people probably assume.

Now let’s start unpacking the details.

What RACK actually owns

THE VERIFIED HOLDINGS, NOT THE NARRATIVE

VanEck publishes daily holdings. As of June 18, 2026, RACK held 51 positions.

The top 10 names account for roughly 42.6% of net assets:

Rolling the full 51-position book up by theme is more revealing than the headline names:

MEMORY AND STORAGE: ~16.8% OF NAV

Micron (5.04%), Sandisk (4.24%), Western Digital (3.48%), Seagate (3.30%), Rambus (0.69%). The largest single thematic concentration in the fund. AI training and inference workloads are driving HBM, NAND, and storage demand, and RACK is positioned for that pricing cycle.

NUCLEAR ENERGY: ~16.2% OF NAV

Constellation Energy (4.49%), Cameco (4.45%), BWX Technologies (2.39%), Oklo (1.66%), NexGen Energy (1.51%), Uranium Energy (1.30%), Talen Energy (0.42%). Functionally, RACK is also a nuclear ETF. Hyperscaler power-purchase agreements with reactor operators are part of the thesis.

SEMICONDUCTORS (INCL. QUANTUM): ~19% OF NAV

Broadcom (4.38%), NVIDIA (4.17%), AMD (2.68%), Marvell (1.30%), Qualcomm (1.24%), Arm (1.07%), Astera Labs (0.93%), Cadence (0.88%), Monolithic Power (0.83%), Synopsys (0.83%), IonQ (0.69%). NVIDIA is large but the basket is more diversified across networking semis, EDA tools, and compute fabric than a pure GPU bet.

POWER AND GRID: ~20% OF NAV

Eaton (4.05%), Public Service Enterprise (3.83%), Quanta Services (2.49%), Cummins (2.42%), Emerson (2.09%), Johnson Controls (1.88%), Ametek (1.36%), nVent (0.71%), Hubbell (0.67%), Generac (0.42%). The biggest individual sector weight in the fund. AI infrastructure is power-constrained, and RACK has more capital here than anywhere else.

DATA CENTER HARDWARE: ~8% OF NAV

Vertiv (3.13%), Dell (2.09%), HPE (1.13%), Celestica (1.09%), Super Micro (0.70%). Cooling, servers, ODM. Surprisingly modest weight given the marketing.

NETWORKING AND CONNECTIVITY: ~8% OF NAV

Amphenol (4.36%), Arista Networks (2.79%), Lumentum (1.05%). Optical interconnect and high-speed networking for the back-end.

DATA CENTER REITs: ~3.5% OF NAV

Equinix (1.62%), Digital Realty (1.01%), Iron Mountain (0.86%). Smaller weight than you might expect from a “data center” ETF. The fund is more leveraged to what goes inside the data centers than the buildings themselves.

The affiliated index provider

THE ONE DETAIL MOST RETAIL BUYERS DON’T KNOW

From the prospectus, verbatim:

“The Index is published by MarketVector Indexes GmbH (the ‘Index Provider’), which is an indirectly wholly owned subsidiary of the Adviser.”

RACK Statutory Prospectus, June 1, 2026

In plain language: Van Eck Associates Corporation owns MarketVector Indexes GmbH. MarketVector designs the rules that determine which 51 stocks belong in the Data Center Supply Chain Index. Van Eck Associates then runs RACK to track that index. Same corporate parent on both sides.

VanEck’s mitigation, also from the prospectus:

“The Adviser has adopted policies and procedures to address concerns of undue influence between the Adviser and MarketVector, including a ‘firewall’ around the personnel that have access to information concerning changes and adjustments to the Index.”

This isn’t unique to RACK. It’s the standard model for thematic ETFs across VanEck, Roundhill, Defiance, and others. The disclosure is appropriate. The structural reality is just worth understanding before you buy.

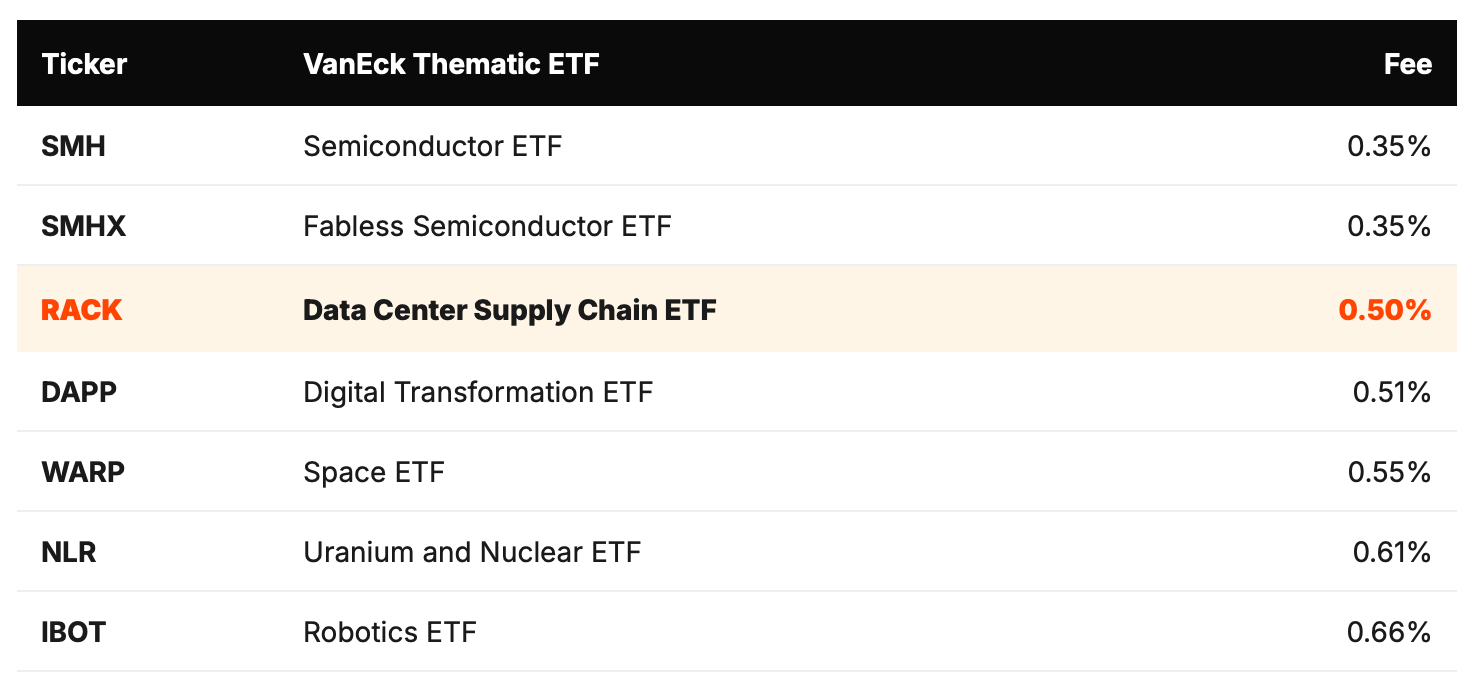

How the fee stacks up

REASONABLE FOR THEMATIC, EXPENSIVE VS BROAD-MARKET

VanEck has several adjacent thematic ETFs. RACK’s 0.50% fee sits in the middle of the lineup:

Compared to broad-market exposure (VOO at 0.03%, QQQM at 0.15%), RACK costs more. On a $10,000 position held 10 years assuming similar gross returns, the cost difference between RACK at 0.50% and VOO at 0.03% works out to roughly $500. That’s the thematic premium.

Bottom line

RACK is a focused bet on the physical infrastructure layer of the AI buildout. Memory, nuclear, power, semiconductors, networking, REITs. Top 10 holdings are about 42.6% of the fund. The structure is clean and the 4x AUM growth in three weeks suggests distribution is working.

Three structural questions worth answering before sizing a position:

Do you want a basket where memory chips (Micron, Sandisk, WDC, Seagate) are the single largest sector concentration at 16.8%?

Does the 0.50% fee earn its keep against building the basket yourself or using two pure-play ETFs (SMH at 0.35% plus NLR at 0.61%, for example)?

The portfolio is real, the structure is clean, and the early traction is meaningful. RACK works as a thematic concentration bet inside a diversified portfolio.

Disclaimer

This article is for educational and informational purposes only. It is not financial advice, investment advice, tax advice, or a recommendation to buy, sell, or hold any security. Nothing in this article should be construed as personalized investment guidance.

Thematic ETFs involve substantial risk, including the potential loss of principal. Non-diversified classification, single-name concentration, affiliated index providers, new fund risk, and sector concentration all add risk above what’s typical for broad-market index ETFs. Past performance does not guarantee future results.

Take on AIPO vs RACK?