Russell Index Reconstitution: The Most Powerful Force in Small-Cap Investing and Most Retail Investors Have Never Heard of It

Tonight at 6pm ET, FTSE Russell publishes the 2026 preliminary additions list. Here's what's actually happening, how money flows during the next 38 days, and which kinds of stocks tend to benefit most

At last year’s Russell reconstitution, $114.7 billion of stock traded on the NYSE in the final minutes of June 27, plus another $102.5 billion on Nasdaq. That’s roughly $220 billion of mechanical, forced buying and selling executed in a few minutes, by passive funds that have no choice in the matter.

This happens once a year. Sometimes the stocks getting added are familiar names. Sometimes they’re micro-cap companies that traded 50,000 shares a day until the moment they were added, and now trade five million.

Tonight, after 6pm ET, FTSE Russell publishes the preliminary list of companies being added to and removed from the 2026 Russell US Indexes. Once that list goes public, a 38-day window opens where stocks on the addition list often see their first wave of institutional buying. By the close of June 26, every passive Russell fund in the world has to own them.

This is the article that explains what’s actually going on.

What Russell Reconstitution actually is

The Russell US Indexes are among the most widely tracked benchmarks in the world. Roughly $8.5 trillion in assets is benchmarked to Russell indexes, with about $2 trillion of that tracking them passively — meaning every dollar in those passive funds has to own exactly the stocks Russell says it owns, in the weights Russell says it owns them.

Every year, FTSE Russell rebuilds the indexes from scratch. Every eligible US-listed stock gets ranked by total market capitalization on the rank day. The top 1,000 become the Russell 1000 (large caps). The next 2,000 become the Russell 2000 (small caps). Together, they form the Russell 3000, which represents roughly 98% of investable US equities.

This is mechanical. It’s not a committee decision. If your company’s market cap has grown enough to cross the breakpoint, you’re in. If it’s shrunk, you’re out. As of the April 30, 2026 rank day, the breakpoint between Russell 1000 and Russell 2000 sat at approximately $5.7 billion, up from $4.6 billion in 2025 and just $1.2 billion in 2009. The boundary keeps moving higher as the US equity market grows — meaning the bar for what counts as a 'small cap' today is roughly 5x what it was 17 years ago.

KEY CHANGE FOR 2026

Starting this year, FTSE Russell is moving to semi-annual reconstitution— one full rebuild in June, plus a smaller November reconstitution. This is the first year of the new schedule, which splits the historical opportunity into two windows but also creates a second one we’ve never had before.

The 2026 timeline

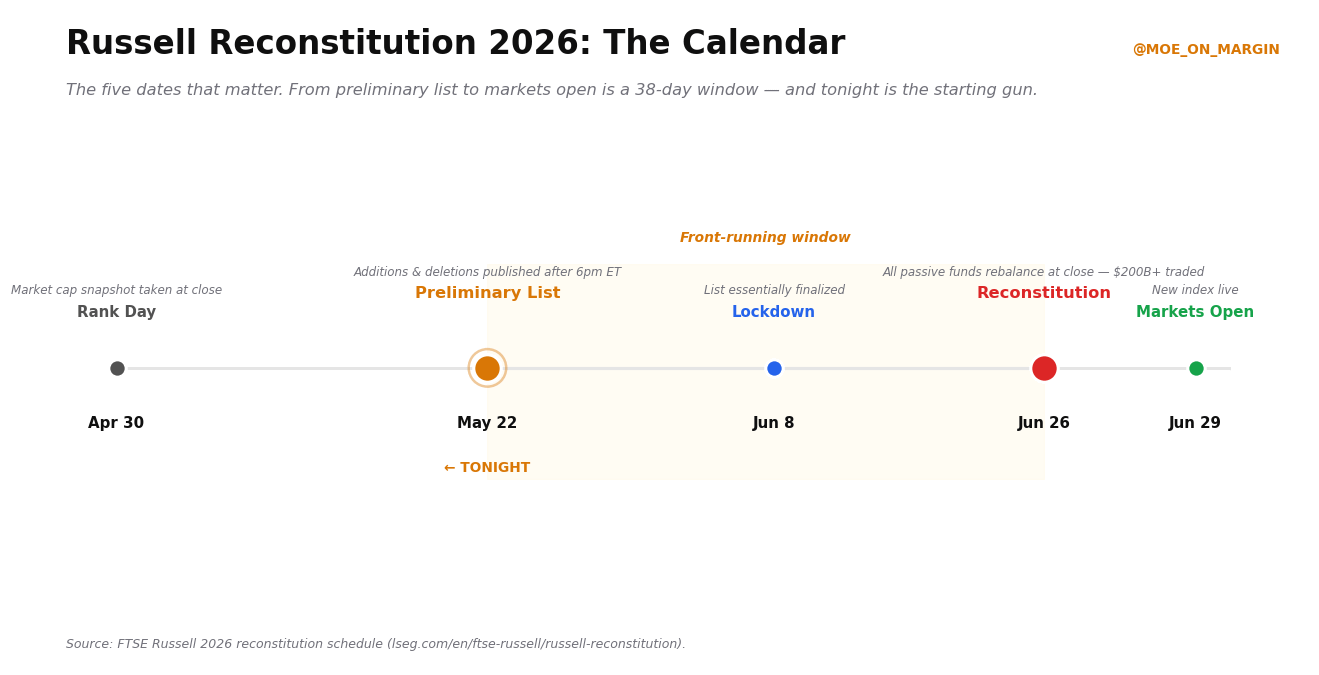

The reconstitution calendar runs over a 60-day window. Five dates matter.

April 30 — Rank Day. Every eligible US stock is ranked by total market capitalization at the close. This is the snapshot that determines who gets in.

May 22 — Preliminary list published. Additions and deletions go public after 6pm ET. The trading window opens.

June 8 — Lockdown. The list is essentially final. Weekly updates between May 29 and June 18 give companies a chance to challenge eligibility, but after June 8 the changes stop.

June 26 — Reconstitution effective. All passive funds rebalance simultaneously at the closing auction. This single close typically prints $150-220 billion in volume.

June 29 — Markets open with the new index live. The new constituents are now permanent fixtures of every passive Russell fund’s portfolio.

What being added does to a company

Getting added to the Russell 2000 is genuinely transformative for a small company. Five effects kick in the moment inclusion becomes effective.

The forced institutional buying is the headline effect. Every passive ETF and mutual fund benchmarked to the Russell 2000 has to own the new additions. IWM alone holds over $70 billion in assets. VTWO, SCHA, and hundreds of other passive funds all have the same mandate. Combined, they create a wall of demand that’s disconnected from any judgment about whether the company is a good business.

Sell-side analyst coverage usually follows inclusion. Stocks that had zero analysts following them often pick up two or three within the first six months. Institutional investors who don’t track sub-$200M companies suddenly have a reason to start.

Liquidity re-rates permanently. A stock that traded 50,000 shares a day can move to 500,000 or higher. Bid-ask spreads tighten. Options markets often open up for the first time. The stock transitions from “hard to trade in size” to “tradeable by funds that actually run money.”

Cost of capital improves. Greater visibility and a higher stock price means the company can raise equity at better terms. Acquisitions become easier to finance. This is a real, tangible business benefit, not just a stock price move.

And short interest dynamics often shift. Many small-cap shorts cover positions ahead of inclusion because fighting forced passive buying is a losing trade. When this happens alongside the buying wave, it amplifies the upside.

How ETFs actually rebalance

The mechanics of the rebalance unfold over four phases, and understanding the phases matters for timing.

Phase 1 — Anticipation (May 22 to mid-June). Active traders and event-driven funds buy the new additions immediately after the preliminary list drops tonight. This is the front-running window. The stock starts moving before any passive fund has touched it.

Phase 2 — Progressive buying (May to June 26). Some passive funds start building positions early to reduce market impact. Volume in newly added names quietly climbs through June.

Phase 3 — The rebalance close (June 26). Every passive fund executes simultaneously at the closing auction. For small, illiquid stocks being added, this single print can be the biggest trading event in the company’s history. This is why $200+ billion of stock trades hands in the closing minutes.

Phase 4 — The hangover (July onwards). Once all the passive funds own the stock, the forced buying is done. Many event-driven traders who front-ran the inclusion sell into this. Stocks that ran hard into reconstitution often give back some of those gains in July. Knowing this is as important as knowing the opportunity.

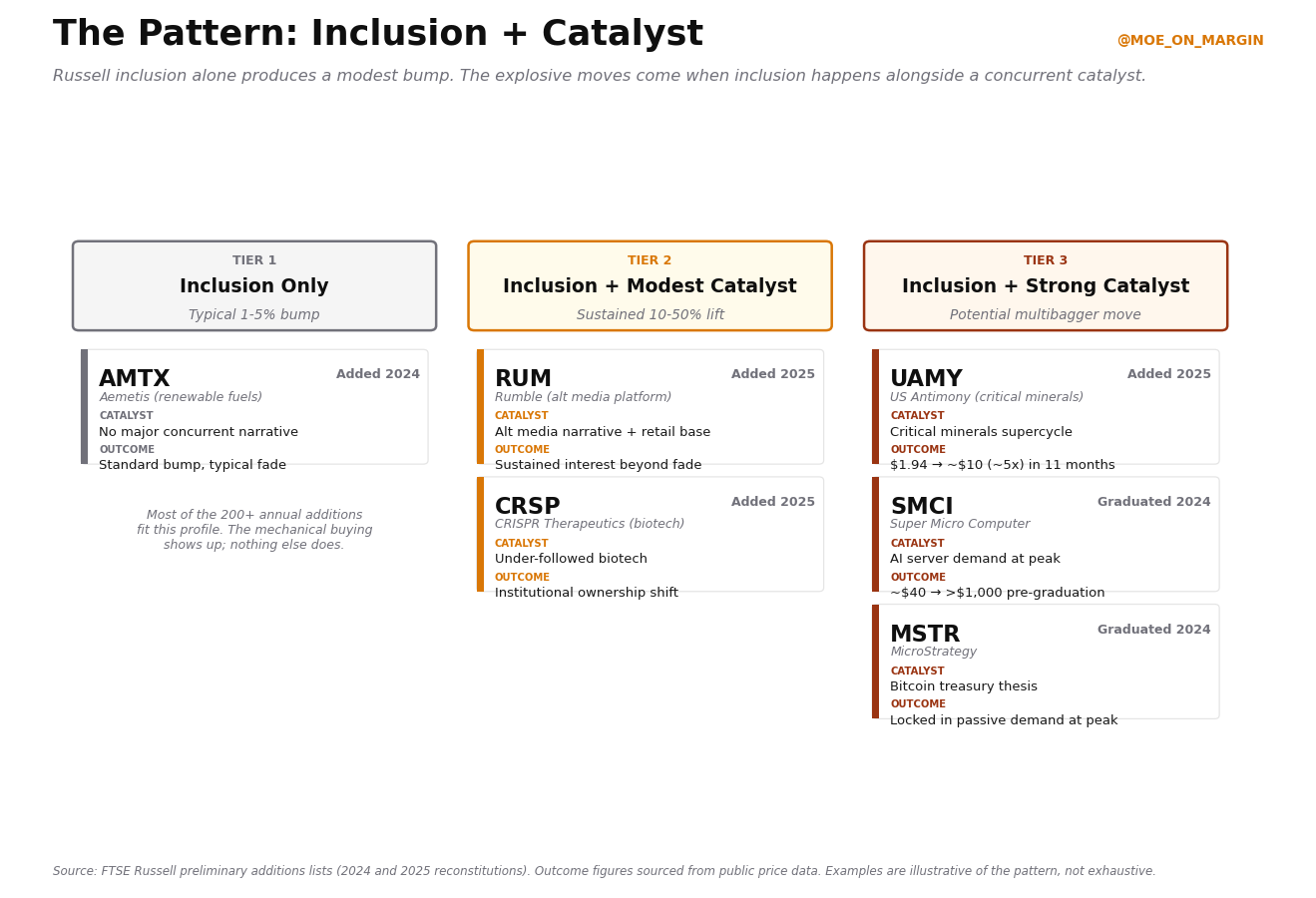

The pattern: inclusion alone isn’t enough

Russell inclusion creates a real, measurable effect on stock prices — academic research from the NBER documents this directly. But the effect from inclusion alone is modest. Most additions see a 1-5% lift over the inclusion window.

The stocks that produce explosive moves around Russell inclusion almost always have something else going on. The pattern is consistent across recent reconstitutions: inclusion delivers the mechanical buying, but the size of the resulting move depends on what concurrent catalysts are in play.

UAMY had a perfect storm of factors compounding the inclusion effect. Aemetis had only the mechanical buying. Both are real outcomes from the same event. Both are reproducible. But they differ in magnitude by an order of magnitude or more.

The screening framework that follows is designed to identify which of these two profiles a given addition is more likely to fit.

The screening framework

If the goal is to find the candidates with the highest probability of becoming UAMY-shaped rather than Aemetis-shaped, the framework is straightforward.

Market cap near the Russell 2000 boundary. Companies between roughly $150 million and $5.7 billion are eligible for the Russell 2000 in 2026. The most interesting candidates sit toward the smaller end of that range, where index inclusion represents a larger proportional impact on institutional ownership.

Low float. A small public float means passive buying represents a much larger percentage of available shares. Under 40% float is interesting. Under 30% is more interesting.

High short interest. Over 10% short interest creates squeeze potential. The mechanical buying forces shorts to either hold through pain or cover. Many cover, which amplifies the move.

Under-followed by sell-side analysts. Names with zero or one analyst coverage have the most room for the “discovery effect” — institutional ownership building once the index inclusion puts them on screens.

Recently uplisted from OTC, or a recent IPO hitting first eligibility. Companies that have only recently become eligible for major indexes haven’t had passive demand baked in yet.

In a sector with concurrent tailwinds. Critical minerals, AI infrastructure, defense, and energy have been the dominant 2026 themes. A name that fits one of those narratives gets the inclusion effect plus the sector wind at its back.

Average daily dollar volume relative to expected passive demand is the final screen. If passive buying is going to represent five times or more the stock’s normal daily volume, the supply-demand imbalance is real and the move is more likely to be sustained.

The risks worth knowing

Not every Russell addition rallies. The most common ways this trade goes wrong are worth listing explicitly.

If a stock has been widely anticipated as an addition for months, much of the move can be priced in before the preliminary list even drops. Buying after the news is sometimes buying the top of a multi-month run.

The Russell 2000 is a rules-based index. It doesn’t filter for quality. Stocks that are burning cash, missing earnings, or facing serious operational challenges get included if their market cap qualifies. Index inclusion doesn’t validate the underlying business.

Post-reconstitution weakness is real. Many additions peak on or around June 26 and sell off in July as event-driven traders exit and the forced buying ends. Holding past the closing print without a fundamental reason often gives back gains.

And the semi-annual change in 2026 is genuinely new. November now matters where it didn’t before, but the historical playbook was built on annual reconstitutions. The first cycle under the new schedule may behave differently than the past 35 cycles did.

What to watch tonight

The preliminary list publishes after 6pm ET on lseg.com under the FTSE Russell reconstitution section. The list itself is the starting point and it seems to be running late on announcement window.

What separates the watchlist candidates from the rest of the additions is the screening framework above: small float, high short interest, under-followed by analysts, concurrent sector tailwind, recent uplisting or IPO status. Cross-referencing tonight’s list against those characteristics is the work of the next 38 days.

FOR CONTEXT

The 2025 preliminary additions list contained UAMY, RUM, CRSP, Talen Energy (TLN), Tempus AI (TEM), Reddit (RDDT), Bitdeer (BTDR), Karman Holdings (KRMN), and 200+ other names. Tonight’s drop is the 2026 equivalent of that document — same format, same publishing channel, same role as the starting gun for the next five-week window.

Russell reconstitution is one of the few moments in markets where you can identify mechanical, non-discretionary demand before it happens. The passive investing boom has made this more powerful over time, not less — more money is benchmarked to these indexes every year. Tonight is the starting gun.

Keep your eyes out for me next article analyzing 2026 additions and sharing my recommendations and rationales.

Disclaimer. This article is for educational purposes only and does not constitute investment advice. Data is sourced from FTSE Russell official disclosures (lseg.com/en/ftse-russell/russell-reconstitution), CME Group market commentary, and SEC filings. Trading volume figures from the 2025 reconstitution ($114.7B NYSE, $102.5B Nasdaq closing minute volume) are sourced from FTSE Russell. The asset-under-benchmark figures ($8.5 trillion total, $2 trillion passive) are FTSE Russell's official estimates as of 2025. Historical examples discussed (UAMY, SMCI, MSTR, AMTX, RUM, CRSP) reflect publicly available data and are presented for educational illustration.

Index reconstitution involves event-driven speculation. Position sizing and risk management matter. Past performance is not indicative of future results. Always conduct independent due diligence and consult a qualified financial advisor before making investment decisions.